About 24% of stocks have outperformed the S&P 500 (^GSPC) over the past two decades, according to Tkr.co. With the tech sector largely reporting better-than-expected results thanks to the generative AI hype, the index has seen a year of record highs. But do earnings paint a full picture of a company? And what does it mean for the overall economy?

Tkr.co Founder and Editor Sam Ro joins Yahoo Finance’s Jared Blikre for the latest episode of Stocks in Translation to discuss how investors should digest earnings. He explains, "When a company beats earnings expectations, that's as much a function of the analyst's ability to estimate earnings as it is the company's ability to beat those estimates or meet those estimates. You know, I think in the short run, there's probably something to extrapolate from that, both from a company's ability to maneuver in the short term as well as how maybe you capture something about analyst sentiment, which might be a reflection of the market participants in there. But I think over the long run, it probably makes more sense to strip all that stuff out and just look at what the actual reported earnings are and see what that looks like quarter over quarter and year over year."

For more Stocks in Translation, watch here.

Video Transcript

Welcome to stocks and translation, your essential conversation for cutting through the market, mayhem, the noisy numbers and the hyperbole to give you the information you need for your portfolio today.

I'm joined as always by Sydney Fried and also a blast from our past here, Sam Rowe.

He is the founder and editor of the ticker.co and he's going to be talking to us about a bunch of stuff, but you were managing director here, managing editor, excuse me of Yahoo Finance back in the day.

Just a quick word for the audience.

Yeah, I was a managing editor of uh Yahoo Finance from 2016 to 2021.

Uh It was a great time, great experience.

I got to work with you very closely and it looks like, you know, the exciting stuff continues here.

This is great like it does, we can uh we're breaking in our brand new green screen here.

So we're gonna put some miles on it on the docket today.

We're going to channel our inner Vince Lombardi and we're gonna get back to fundamentals.

In other words, earning sales and the like what investors should take away from these key quarterly numbers and our phrase of the day, the bottom line, what it means for corporate profits, as well as your portfolio.

And this episode is brought to you by the number 24.

That is the percentage of stocks that beat the S and P 500 this century.

Just one in four.

I know we're gonna tell you why that's good and bad news for investors.

Sam Sidney first, the story of the week, we're talking fundamentals here and that would be revenue net income gross margins and this is your wheelhouse and this is how you look at the market, just kind of break that down for us and what you're seeing right now in the market.

Yeah, I mean, you know, we always see what the price action is looking like, you know, for, for the stock market S and P 500 dow and the individual tickers and you know, all the fluctuations and stuff can be kind of nerve wracking, especially when you see a huge run up in price or a big drop or whatever.

Um But you know, I don't think price alone is what, you know, investors should be thinking about because at the end of the day, over time over the long run, at least price seems to be driven by the fundamentals and most importantly earnings.

And so I guess that's what we're talking about today.

Yeah, and I just want to differentiate, you're talking about market prices and prices of stocks are really the domain of technical analysis and that's really what my specialty is.

So fundamentals, I would say can complement technical analysis.

But I mean, how do you look at it for sure.

I mean, yeah, they absolutely do, do compliment.

And I think you're right.

Like, I think, uh, in my experience it seems that, um, you know, technicals can define short term moves much more uh uh than the fundamentals.

Um You know, if the fundamentals uh uh drove prices and, you know, the markets would always be efficient, there'd be no opportunity we had.

Um But yeah, I think that's sort of, I think that's the sort of the right balance.

So Sam, if you're kind of an early investor, I think it's clear you could easily look at a stock chart and say this stock is up 50% this year, like why not just invest?

But you look at the fundamentals, that's what we're talking about.

What's the most important fundamental.

We should be watching revenue net, whatever.

Yeah, I mean, I think, I think it all comes, I mean, you know, it's the bottom line, right?

Um And, and I think we're talking about this just a second ago.

So, you know, people throw around the phrase the bottom line all, all the time to get to the conclusion to the main point.

But the etymology, the story behind the bottom line is it's actually an accounting term, right?

You know, back in the day when people used to have these big paper ledgers and write out their income statements.

You know, the very top, the top line is sales, the revenue, right?

How much money comes in from actually selling sales and revenue mean the same thing.

A lot of stuff.

Yeah, a lot of stuff, sales revenue top line, it's all the same thing.

And then once you adjust that for the costs of, of, of those goods or services, you take out all the expenses, you take all the interest expenses from all the financing, you take out the taxes and other random things, then you have net income or earnings or as they say in the accounting, uh practice, it's the bottom line.

So, so yeah, that, that's what it always gets back to because at the end of the day, you know, you start a business, you invest in a business.

Um sure, like maybe philosophically you're out there to sell a really great product or service.

But as an investor, it's about how much money you can actually make from that investment.

And the money you take home is that bottom line.

You know, everything that, that after all of your costs and expenses.

Yeah.

You know, I think people have asked.

So let me just back up and say there are, there are a couple of different things that really drive the market and one of those arguably uh is interest rates and that's something I pay attention to the fed.

I think most people do, but it's really about earnings and maybe just kind of break down the import that if you don't have earnings growth eventually, you're just not going to see stock market returns.

In other words, the stock price is not going to appreciate.

Sure.

Yeah, because, you know, the stock price is going to be sort of in one way or another, uh, related to where earnings are.

So if earnings are going sideways and you can't really expect the stock price to move up and you know, people will seek other kinds of investment opportunities.

Is there like a way in terms of a company's earnings?

Oh, this company had beat earnings expectations 10 times in a row.

That's a good company to invest in.

Is there a hard and fast rule for something like that?

Yeah, I mean, I think that's really tricky because, you know, when a company beats earnings expectations, that's as much a function of the analyst's ability to estimate earnings as it is the company's ability to beat those estimates or meet those estimates.

You know, I think, you know, in the short run, there's probably something to extrapolate from that both from, you know, a company's ability to maneuver in the short term as well as you know, how analysts, you know, maybe you capture something about analyst sentiment, which might be a reflection of, of, you know, market participants in there Um, but I think over the long run it probably makes more sense to, you know, strip all that stuff out and just look at what the actual reported earnings are and see what that looks like.

Quarter, over quarter and year, over year, um, over time and what's expected in the quarters and years to come.

You know, when we look at earnings, um, they can, the various metrics can change by a company according to their industry.

For example, Walmart might be looking at gross um gross merchandise volume, but all companies report sales, that's that top line.

All companies report profit.

Um and then you have adjusted and, and then you start getting into all these different, you know, variations on a theme here.

Is it possible to get an apples to apples comparison or is it just always going to be apples to oranges?

I think it's kind of always going to be apples to oranges.

If there are one really great bulletproof accounting standard that everyone would be happy with, then there would never be a does not exist, it does not exist.

And it's actually something that, you know, legendary investor Warren Buffett writes about almost every year in his annual letter, you know, when he reports um Berkshire Hathaway's quarterly earnings, they always report the gap the generally accepted accounting principles, um earnings and net income figure.

But he also knows that that standard requires them to report these massive swings in their equity portfolio where, you know, on paper, the value of the company and the value of their investments might be going up and down.

But if they're not never selling this, then it's actually not realized.

So they have a lot of unrealized gains and unrealized losses in a given year.

And so, you know, you don't have to really worry about what all that stuff means.

But the, the point of that is uh you know, Warren Buffett and Berkshire hat way for instance, will make an adjustment for that, you know, they uh remove all the, the noise that comes from stock price fluctuations and give you what they call an operating earnings number, which, you know, some people will call an adjusted number or the non gap number.

Um And the thinking behind that is by taking out some of these things that are noisy or um you know, unusual items, you get a better sense of the underlying health of a company.

But Sam a lot of what you're saying, I think must be really using for an early investor.

Someone who does new investors like a lot of these terms are similar, the gap non gap, the profit, don't we say adjusted eps and profit are like the same thing.

This is a different, yeah, it creates all kinds of confusion there too.

So how do you cut through that language?

Even when someone is trying to simplify something for you?

I mean, well, yeah, I mean, that, I think that's the real question, Jared.

Like, can, can you actually cut through and it's like there's a certain point where you can't simplify it anymore because at the end of the day, investing is complicated.

If this was easy, then everyone would be doing it without thinking twice.

And, you know, we frankly, we'd probably be out of the job.

Right.

Because, I mean, I definitely would too because if people understood this, you know, I mean, I think there's a lot of people, there's an investing class that, that has a good grasp of this.

But, you know, I think for us, you know, people in the finance media industry where we are involved in education, you know, we do have to try to figure out new ways to make this interesting and approachable and, you know, you also have to add this whole other layer of stuff like accounting standards are changing constantly.

Yes, that's another one.

Yeah.

So accounting costs are always going up, right?

And the accounting costs go up and then, you know, it's like that's its own entire industry.

Um So, yeah, I don't think there's really a, a great way to oversimplify or, or to simplify it in a way that's super intuitive.

But I think a good starting point is to actually just, um, you know, listen to what a company says about their earnings or their net income.

We see a lot of cross currents in the market.

And this is a term that you've specifically used in some of your recent newsletters.

What do you see as the cross currents right now?

Because some, a lot of times in the market, seemingly, always, one group of things is saying is going this way, another group of things going that way and then maybe the market goes that way.

Sure.

Yeah, I mean, I think there's a couple of different things that, um, to juggle as someone who's following the market or following the economy and, and sort of the interplay between all those things.

So one thing that's, you know, already kind of confusing is sort of the trajectory of the economy, right?

Like, uh, you know, for the last couple of years, we've had a pretty high pace of growth, uh fueled by a lot of spending a lot of consumer spending, retail sales, industrial activity, um people going back to work, um, the economy reopening and GDP, you know, is accelerating and all this kind of stuff.

Um, more recently it looks like growth has been decelerating while, you know, stuff like retail, like all these things we just talked about might still be growing, the rate at which they're growing is sort of cooling down a little bit.

So I think that's like one of the bigger stories that, that uh we're sort of reading more and more about is that the economy is slowing now, is that necessarily a bad thing um you know, sure, if, if you're, if you were positioned in a way, whether you're an investor or you are a manager at a company, if you're expecting a really high pace of growth and you invested for that, then yeah, maybe you're in some kind of trouble.

But I think the important thing is that the economy continues to grow and, and the businesses operating in that environment are continuing to see sales grow as well.

So, um yeah, it's confusing but yeah, we're going from, you know, a really great pace of growth to more, you know, decent, moderate pace of growth and um you know, sometimes slower just seems like it's going in the reverse, but that's not actually the case.

We need to pause right here just for a second.

We're taking a short break, but coming up, we're going to break down a surprising finding about long term stock holdings and another episode of who wore it better.

All right, we are back and if you're keeping score here, we already went through our phrase of the day here.

The bottom line we've defined actually Sam defined that for us in our opening segment here.

So we are moving on to the episode.

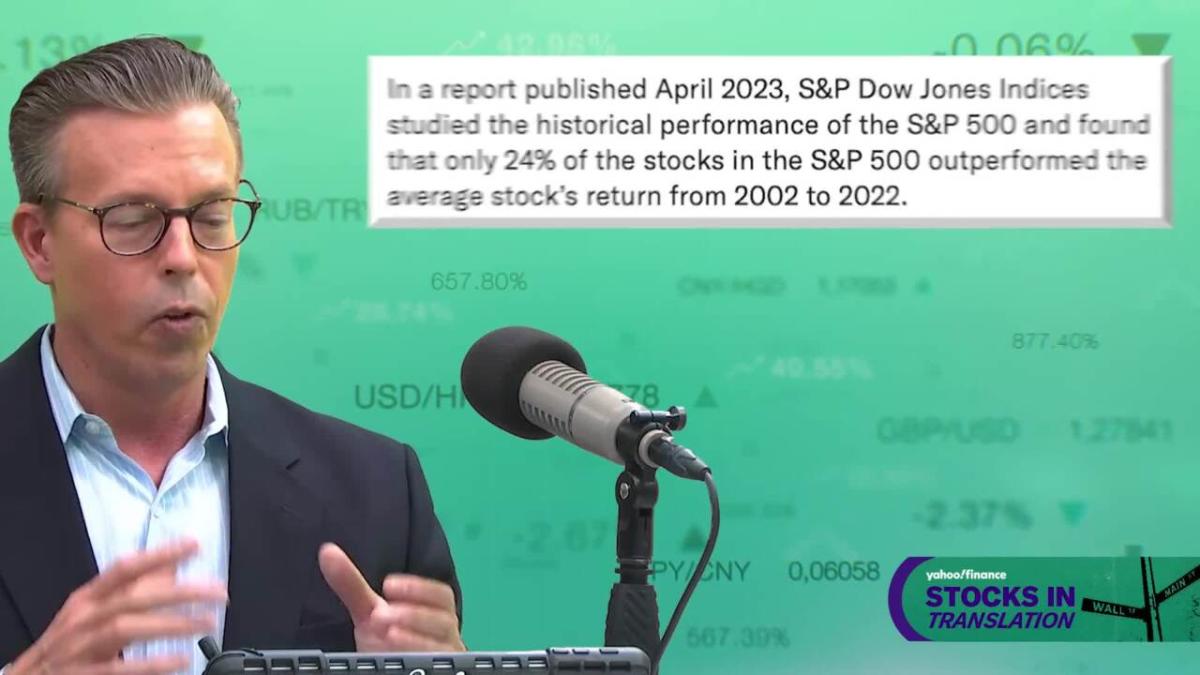

This episode is brought to you by the number 24 and you might be surprised to learn that only 24% of the stocks in the S and P 500 outperformed or had a higher return than the index itself.

That's the S and P 500 which was up 390% over this period.

That's 22 years.

But Sam, only one in four stocks outperformed.

That means 75% of them did not.

If you're investing in the S and P 500 you're, you're ok.

But if you're stock picking seems like you might lose, miss the boat there.

Yeah.

I mean, you know, the odds are stacked against you if you're trying to pick winners in the stock market or, or I guess more specifically trying to find the stocks that are going to outperform the averages, outperform the index.

And that's not what I want to hear.

I want to hear that I can pick.

Yeah.

You know, I mean, the, I guess the easy sort of like, I guess there, there used to be this myth out there that you could flip a coin or, you know, you can have monkeys throwing darts at a, at a stock sheet and, you know, because it's kind of 5050 there was a decent chance you can find the stocks that are going to beat the market and help you become more rich than someone who's just invested in S and P. But, um, there's been a lot of really great studies that have been published in the last couple of years.

The one you're talking about comes from S and P Dow Jones actually.

And what they did was they did a study of um uh the S and P 500 return as well as the individual components of the S and P and yeah, it turns out that it's a small handful of, of, of, you know, a quarter or maybe 20% of the stocks um in the index actually outperform.

And one of the reasons why um this happens is because of asymmetrical returns, right?

Or asymmetrical performance, right?

A, a specific company can only fall by 100%.

But on the way up, you can go up 100 203 104 100 it can go up for infinity.

Um You know, there was just a great Bloomberg article last week that was published, I was talking about since Nvidia's IP O, NVIDIA is up 350,000%.

Like these are astronomical numbers.

So think about 510 baggers are embedded in there.

That means five times it has experienced 1000% returns over a relatively short period of time, right?

So like unless you're smart enough or lucky enough to actually pick that those right stocks, um if you don't have those in your portfolio, then you're going to underperform no matter how great of an investor or stock picker you are.

So, you know, the takeaway ends up being that, you know, unless you're convinced that you can have some kind of advantage in this market, the move ends up becoming, you know, buying the entire index because you're also going to get exposure to those winners that are going to drive the entire market higher.

So what is, what is, what do we really mean by outperform?

Like obviously, it means a stock does better than the whole of the index.

But there's a lot of ways we say outperforming, we rate stocks, outperform, we rate them like and then it's like once, once you're outperforming, aren't you just performing?

So that's one of the great, it's, it's so confusing, like, especially like when, when analysts on Wall Street rate stocks because everyone has kind of a different convention.

There's, uh, there's outperform and underperform, there's buy and sell and some places will actually say overweight and underweight as their way of communicating.

So there's sort of like two categories of this.

Um, there are the absolute ratings and, and the relative price ratings.

So absolute meaning, um, you know, is the price gonna go up or down.

So this is where you have company or, or firms that say, you know, you either buy hold or sell a stock because they think it's either gonna go up nowhere or down outperform or underperform is a way of communicating that they think that uh, a stock that's gonna outperform is gonna do better than average.

A stock that's gonna under perform is gonna do worse than average.

So in this universe, it's actually possible for a stock to be going up, but if it's going up at a below average pace, it's underperform.

It might sound bad.

But you could still be making money on this.

It sounds confusing.

But I do kind of like, but it's s, and P 500 people have price targets but they don't have the buy, I mean, that would be weird.

Right.

You can't buy the S and P on its own.

So, buy outperform like no one's doing that.

I mean, you can certainly, you can certainly, I mean, it's some people do, some people don't.

Um, it is a popular practice for, for various Wall Street firms to have a target for the S and P 500 as an index.

Um, and through that they're communicating whether you should be buying or selling.

Um, but, you know, I think something that, you know, you learn over time after paying attention to this for a little while is that a lot of times those price targets are very, um, are off.

Yeah.

Well, sometimes, I mean, sometimes it looks like somebody just chose those with, uh, a dart.

I, I mean, there's a whole, there's a whole game to analyst ratings in and of itself.

Um, but, you know, you're always trying to guess what this company is doing in its own, you know, behind the doors, black box model, their black box model.

So it is difficult to divine what's going on.

Sure.

And, and, you know, it's not, and, and the, the, the confusion actually ends up going both ways, right?

Even if you do have a pretty great grasp of what a company is doing and what that business is doing and you come up with a number that, that, you know, may or may not be in line with what that company's management is thinking.

Well, you know, if, if your target for earnings, for instance, is not in line with management's internal targets for earnings or what, what they're on pace to do, then the companies themselves might feel under pressure to, you know, maybe move some things around in their business to meet what the analysts are, are suggesting.

Um, this company should earn.

So, yeah, it's, it's a, it's a really fraught, uh, game that, that we play every quarter where, you know, did this company actually meet or miss expectations or are they, you know, pulling some tricks to, you know, uh, be, or miss those expectations?

Yeah.

And, and, you know, what are the analysts doing too?

It's like, is this a matter of, um, uh, you know, trying to actually be accurate or are they trying to come up with numbers that might be a little bit below, um, the averages so that the company just want to get headlines?

I mean, we see everything, of course.

Yeah.

Yeah.

All right.

We're gonna leave that for a second and we want to make time now for who wore it better where we stack two things or ideas next to each other to come to a no unbinding opinion about who's wearing it better.

And Sam today we're, we're looking at two different Warren Buffett quotes and we want your opinion about which one deliver delivers a better, more useful message to investors.

So, and both concerned prices, by the way, quote.

Number one, Warren Buffett, it's far better to buy a wonderful company at a fair price than a company at a wonderful price.

Number two, price is what you pay value is what you get.

So, two different ways of looking at it there.

Uh, I feel like they kind of mean the same thing.

So I'm, I'm, I'm gonna go with the second one because it's a little bit more straightforward.

Um, price is what you pay.

Like, you know, that's very intuitive and value is what you get.

Um, you know, the, it's like buying a cup of coffee at Starbucks or whatever, right?

You pay $8 to get a venti coffee and, you know, you know, that's the actual transaction but, you know, maybe you get, you know, $15 worth of joy out of it.

And so that, that's the value, right?

It's like it gains of, uh, you know, of that Amaretto.

Yeah, I mean, like if my, if my mother, you know, goes to Starbucks and pays $8 for that coffee, she's getting $4 worth of value out of it.

So, it's a completely different, you know, the nature of that.

She's not there in the first place, probably.

Exactly.

Yeah.

So, so I do like that quote because it makes you think about the difference between, you know, one type of dollar sign versus another price is what you pay value is what you get.

Uh, we got some time left.

I want to talk to you about your personal journey.

Here.

You left Yahoo Finance, I believe in 2021.

Correct me if I'm wrong, but you started the ticker.

Uh This is your own newsletter.

This is your baby.

You put your heart and soul into it.

Tell us what, why you started it and what you wanted to give to investors.

Yeah, I mean, you know, the simple, the simple thing is it's, it was based off of a lot of feedback that I felt like I was getting from readers um over the years uh throughout my career of, of doing this for about 15 or 16 years where, um you know, I think there are, you know, the the big, big audiences are made up of lots of different small audiences, right?

Um And I think that there was, I had some kind of a following or I was getting feedback from people who like a certain kind of storytelling or like a certain kind of coverage that um they were getting at, at places like Yahoo Finance or, or, or whatever.

Um And so it's for an audience that's a little bit more longer term thinking, um, that might not be as active in their investments.

Um, as someone who might be like a retail trader or someone who does, you know, follow the markets every day.

Um, you know, I write for an audience that I, I think that's, that's pretty much it, you know, longer term thinkings, you know, people who, uh, do see headlines every day but they wanna know what those headlines mean in the context of them planning for retirement in 20 years.

Um, you know, uh the same story or the same development in, in corporate America or the economy will mean different things depending on your time horizon.

And so for, for my audience, it's mostly about, um, people trying to understand what things mean in the long run and that's hard because it's hard to, we talked about this earlier.

It's hard to digest all these different languages that make up the stock market, right?

So what would you say your audience?

I don't know if you have this information kind of struggles to understand about the markets or about their portfolio.

I mean, I think, I think it's, it's less about the understanding and more about, um, sort of separating material news versus the noise and not to say that there's any kind of, you know, news that isn't newsworthy, but there might be news and there might be developments that might not be material for someone who's thinking in the long run, you know, kind of like what we were talking about earlier about, you know, what, whether or not a company beats or misses earnings estimates.

Right.

You know, that might tell us something about the market action in a given day or a week or a couple of months.

But behind that you have this net income number, the bottom line.

Right.

The word of the day, there's a lot that we're not seeing.

Yeah, there's a lot that's not, we're not seeing and it can be pretty, um, you know, depending on the audience, it can be pretty distracting to see a headline that's, you know, this company beat or missed expectations.

Whereas it might actually be the case that a company that's missing expectations is still delivering earnings growth and still continues to plan to deliver earnings growth.

So, you know, that's the other side of it like II I try to approach things with a certain kind of framing with that sort of audience in mind.

Yeah, go ahead.

I was just going to say and what do you think like in your own financial journey?

What do you think has been the hardest thing to understand?

I think the hardest thing to understand was actually what we were just talking about this idea that yeah, we covered it.

You know, the, the idea that picking stocks is like a coin toss when in fact, you know, picking winning stocks is, you know, the odds are stacked against you.

Um, you know, unless you have some unique skill and which, by the way, there's an entire industry of people who get paid tons of money to try to figure out what these winners are and almost all of them underperform and pick the wrong stuff.

They're not doing.

The hedge fund managers are not doing a great job themselves by and large.

Exactly.

So, I think that's what took me the longest to sort of understand, at least for, for myself in, in terms of my own investment philosophy is that, um, you know, it's very difficult to, to beat these indexes.

So you just what I love about the ticker, you're always coming from an honest place trying to break things down for people.

You ask the questions that are always in the back of my mind, but don't seem to get addressed, my only paid sub, I get nothing out of this.

But, uh, you're, you're one of the greats here.

So, continued success at the ticker and we are, we are winding things down.

24 minutes, goes pretty shortly here.

But thank you, Sam, once again in Sydney as well.

Keep it locked to Yahoo Finance.

No comments:

Post a Comment